VAT was introduced in UAE on 1st January 2018.

VAT registration is a mandatory step for companies and individuals doing business in the UAE. For taxable supplies, the supply of goods or services made by a business in the UAE is taxed at a rate of either 5% or 0%. Imports are also taken into consideration for this purpose.

Your company is eligible for VAT registration based on the following terms:

Mandatory Registration

- Registration is required for free zone and mainland companies with a turnover of over AED 375,000.

- The company should register in the case of the total value of their taxable supplies made within the UAE exceeds the mandatory registration threshold mentioned.

- Registration is required if the company anticipates making taxable supplies with a value exceeding the mandatory registration threshold in the next 30 days.

Voluntarily Registration

- If the company has an annual turnover of between AED 187,500 and AED 375,000, it’s then voluntarily to register.

- Voluntary registration is applicable for companies with a total value of taxable supplies or expenditure in the last 12 months exceeds the voluntary registration threshold.

- Voluntary registration is also applicable if companies anticipate a total value of their taxable supplies or expenditure in the last 12 months exceeds the voluntary registration threshold.

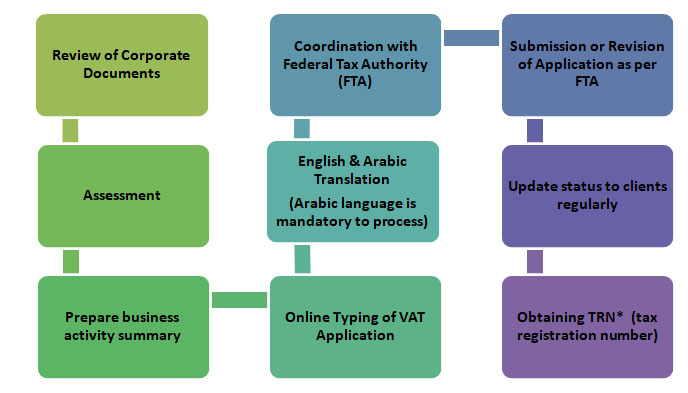

VAT Registration process

* Issuance of Tax Registration Certificate solely and completely depends upon the approval from FTA

Note: Failure to complete the registration on time will lead to a penalty of AED 20,000

Get VAT Return Filing Done By a Beehive Tax expert

VAT Return Filing – is a submission of an official report detailing taxable purchases and sales made by the Taxable person. VAT Return should be completed either by a Taxable Person, their legal representative or a Tax Agent and submitted online to the Federal Tax Authority (FTA) as per the schedule assigned by FTA, but no later than the 28th day following the end of the Tax Period (which is either one or three months).

With respect to sales

- Supplies of goods and services made which are subject to the standard rate

- Tax refunds you have provided to tourists under the Tax Refunds for Tourists Scheme, if you are a retailer and provide tax refunds to tourists in the UAE under the official tourists refund scheme

- Supplies of goods and services received by the Taxable Person which are subject to the reverse charge provisions

- Supplies of goods and services made which are subject to the zero rate of VAT

- Supplies made which are exempt from VAT

- Goods imported into the UAE and have been declared through UAE customs

- Where applicable, adjustments to goods imported into the UAE and which have been declared through UAE Customs.

With respect to purchases

- Business Purchases and expenses that were subject to the standard rate of VAT

- Any supplies which were subject to the reverse charge for which you would like to recover input tax.